What do funding rounds look like for AI startups?

What does a Series A really mean these days?

People often use the names of funding rounds as shorthand for a company’s maturity level. A “Seed-stage” company is very early in their journey, often with fewer than 10 employees. A “Series F” company is likely very large, and is probably actively considering going public in the near future.

Staged investing rounds exist so that investors can control their risk: a very early company is very likely to fail, and as such is only given a small amount of money to experiment with. As a Company matures and “de-risks”, it raises money at increasing valuations, to adjusts for its changing risk-reward profile.

But how does a Company “graduate” from one stage to the next? Is there an official rubric, sets of KPI’s, or revenue threshold that a Company must clear to raise a new major financing round?

While unsatisfying, the short answer is no.

The reality is that the stage names are largely VC marketing (value-add!) used to loosely indicate a Company’s level of maturity. Unfortunately, these are largely subjective, and differ meaningfully from one industry to the next. One can imagine that the “signs of maturity” look very different for a BioTech business than they would for a Consumer social app.

As a starting point, however, I think the below graphic is helpful (from the Asper Brothers / MintyMint)":

Generally speaking, most investors historically agreed that the “Series A” funding round is the one in which an outside investor has agreed that a Company has now achieved “product-market fit”.

There are a million and one interpretations about what that means, but I think of it as being the stamp of approval that a company’s product has been proven to satisfy a major need in a market. Once again, this definition is subjective and challenging to prove mathematically; another reason why early stage investing is often closer to an art than a science.

For those desperate for a benchmark, VC’s often use the a hurdle of “$1M of ARR” to describe product-market fit. Again, this differs significantly depending on the market, so it can be taken with a grain of salt.

Any funding round prior to a Series A is often interpreted as some sort of “Seed” round, whether it be called an incubation, pre-seed, angel round, seed round, seed extension, Seed-2, pre-Series A… the list goes on. The reality of these names is that they’re all various forms of VC marketing and really mean that a Company has yet to prove PMF, but needs to raise more money to do so.

Any funding round after a Series A has traditionally been thought of as a Growth round: the business model works, but they company needs more capital to go execute on things and grow (often by investing in Sales & Marketing). Subsequent major funding rounds will graduate to the next letter (e.g., B→ C), but there’s not really anything that differentiates growth stage companies at this point: the only real difference between a Series D company and Series E company is the number of major funding rounds they have announced.

How does this differ in the land of AI?

As anyone close to the AI funding world probably already knows, the above milestones have so far not applied to most AI companies. While there is a lot of excitement in the market today, the reality is that very few AI companies have actually proven product-market fit (let alone proven sustainable unit economics).

Furthermore, most of these companies are more capital intensive than traditional software businesses, and have to raise more money to get a product out into market that what we’d see in traditional software.

Taken together, the current wave of AI startups has proven to look very different than the proliferation of SaaS, mobile, and cloud-first startups of the last generation.

Even the term “AI startup” is way too broad to be helpful.

Are we referring to company’s that are literally inventing new forms of AI / pushing the field forward (e.g., Cohere, OpenAI, Anthropic), company’s that are building on top of underlying AI platforms (e.g., Jasper, Copy AI), or company’s that are integrating AI into their already existing software offerings (e.g., Notion, HubSpot)?

What about companies that are providing the underlying compute needed to power AI businesses (e.g., CoreWeave, Together)?

In addition to looking different from the prior waves of startups, AI startups have proven to look increasingly different from one another. Everyone prefers simplicity, but the reality of the situation is that investors have to look at every subcategory of AI startup differently.

Proposing a framework for AI startups

At Radical, we typically think of AI companies as first falling into one of two buckets: “AI-first” or “Applied AI”. AI-first companies are literally inventing new AI. Applied AI companies are leveraging best-in-class AI solutions to go solve problems in unique ways.

Again this can be fairly subjective, but I think it’s a helpful framework. These types of companies look completely different internally (e.g., researcher-heavy vs. engineer-heavy), and often have very different goals.

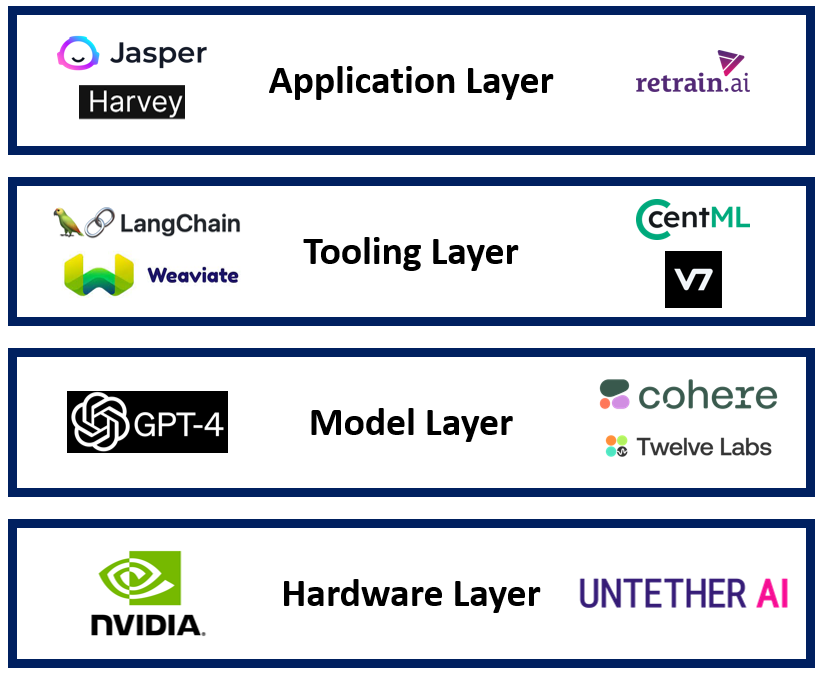

Beyond a Company’s north star / relationship with AI research, one must also consider where the company plays in the “AI stack”:

Companies that are “higher in the stack” are closer to end markets and customer problems themselves, while companies “lower in the stack” are enabling companies in the layer above them. For now, we will exclude the Hardware layer, which really tends to play by it’s own rules.

Generally speaking, model layer companies are likely to be AI-first, application layer companies are likely to fall into the Applied AI category, and Tooling businesses can go either way. As one might expect, however, there are many exceptions to this rule (not the least of which are companies that play across multiple layers).

As we spend time with companies across the spectrum, we’ve noticed that signs of maturity and success look very different across the board. Below is a quick summary of how I’ve been thinking about what different “signs of maturity” look for companies of various stages:

It goes without saying that the above is overly simplistic, but I think there are a general lessons to take away:

Implications

There is no “one-size fits all template” for venture funding rounds: every subcategory of Company has it’s own KPI’s / benchmarks, and this has proven to be even more nuanced for AI companies

Application Layer AI companies are generally assessed similarly to traditional Enterprise SaaS solutions of old, but (for now) seem to be given a bit more leeway around revenue targets (i.e., can raise at higher multiples / less revenue) than non-AI companies

What’s more important than a revenue threshold is that sales motions are clearly repeatable: are there multiple customers who you can target in consistent and scalable ways (as opposed to just having one-off relationships)?

Tooling Layer businesses generally tend to fundraise one stage behind Application Layer businesses, as they take a but more capital investment and time to get them running.

This seems to be the most common layer for Open Source businesses to participate in: oftentimes a Series A for these companies will still be pre-revenue, but post active community and customer deployments

Model Layer businesses tend to raise on entirely different technical thresholds, given the levels of capital intensity that they require. There is a strong belief in the investor community that these will be great businesses in the long run, and as such, get away with showing less customer traction in the early innings

We discussed this at length a few months ago

For startups, it’s important to identify which category you’re building in, and then set your expectations / assess competition accordingly

In other words, if you’re building an Application Layer business, you should expect to have to show real revenue growth and raise at valuation multiples in your zip code

On the bright side, these businesses can generally move much faster and be much more capital efficient

Many of the craziest funding early rounds in AI are driven by the need to pay for compute to train models, and are not necessarily an indication of business quality: they’re simply the cost of doing business

Agree? Disagree? I’d love to hear from you if you’re hearing something different.